Running a construction business gets messy real fast. With long pay cycles, large sums of cash being tied up in materials and labor on top of already slim margins, there’s very little room to make up for costly mistakes. That’s why you need solid reports so they can keep a pulse on the health of their business and catch issues before they put you out of business.The trouble is, creating a solid reporting system isn’t as easy as throwing some numbers into a spreadsheet and adding some fancy formulas. No, you need a process for data collection and know how to translate all the data your reports are giving you. And before all of that, you need to know which reports are worth putting the time into creating and maintaining.

The reports we’ll walk through aren’t just paperwork, they are the foundation of your business. To ignore them would be like ignoring a crack in the foundation — get them wrong, and put everything built on top at risk. The good news is, you don’t need to be a certified accountant to get a handle on these. And while there are many reports that are helpful in running a construction business, we’re going to run through some of the most common.

First off, why these traditional reports over simple metrics?

- Depth of Insight: Your bank balance tells you how much money you have, but it doesn’t tell you if you can afford to hire another PM. These financial reports give you the full picture so you can make informed decisions about the future of your company.

- Risk Mitigation: Ever had that gut feeling that something’s off? These reports will validate that gut feeling with facts and figures you can act on.

- Future Planning: Simple metrics are snapshots; they don’t show trends. Financial reports are your time-lapse camera, capturing trends in how your business is growing (or stalling).

- Accountability and Transparency: Whether it’s your team members, stakeholders, or future investors, standardized reports are the universal indicator of your business’s health.

Now let’s dig into some reports you’ll want in your arsenal.

3 Accounting Reports Contractors Must Understand

Tech changes how we work, but some tools, like these reports, stay the same because they keep business owners tuned into their financial health. Take a look at this diagram. It breaks down the essentials, giving you a clear view of how everything ties together in your finances.

Let’s walk through those three crucial reports.

Cash Flow Statement

- What is it? Cash is king. This report tells you where your money is coming from and where it’s going.

- Why bother? This is your operational pulse, keeping tabs on the lifeblood of your business—cash. It’s like the logistics of getting materials and labor on and off your sites; if the cash isn’t flowing, nothing else will either.

- How often should you check it? Monthly, or even weekly if cash is tight or when you’re considering major expenditures like new equipment or additional hires.

Income Statement (AKA Profit & Loss)

- What is it? Shows if you’re making money or losing it.

- Why bother? Consider this your project’s post-mortem but for your entire business. It tells you if you’re actually making money or if you’re working just to break even.

- How often should you check it? At least monthly, and definitely before making large financial decisions like scaling up your workforce.

Balance Sheet

- What is it? Gives you the big picture of your financial stability.

- Why bother? Before digging a foundation, you’d check the soil, right? You’d test for clay, sand, silt—make sure it’s not a swamp. The Balance Sheet is like that comprehensive soil test. It tells you if you’re building on financially solid ground or quicksand that can pull your business under.

- How often should you check it? Quarterly, any time you’re considering taking on more debt or before a large project kick-off.

Common Types of Construction Reports Contractors Need

Once you have the standard reports in place, it’s time to build reports that address financial situations specific to construction companies, whether you’re a general contractor or a subcontractor. This is where things get hairy, because most generic reporting software doesn’t support these types of reports natively. But don’t worry, we’ll walk you through how to build them and get all the data you need.

WIP (Work-in-Progress)

- What is it? Gives you a bird’s eye view of how cash is flowing across all your current and backlogged projects, taking into account each project’s timeline and invoicing patterns against a particular project’s budget and timeline status.

- Why bother? This report combines data from the office and the jobsite to give you an accurate picture of how your projects are doing, and shows you whether or not you need to change direction. It also should give you a glimpse into what your cash flow might look like in the future and how you should allocate your resources.

- How often should you check it? Weekly, depending on how many projects you have in progress.

Historical Profitability and Overhead Analysis

- What is it? Analyzes your margins, overhead costs, and overall net profits from previous jobs.

- Why bother? With this data, you can bid with a markup that’s proven successful in the past and have a better chance of achieving the profit margins you’ve projected. It will also show you what type of projects and clients produce the most profitable outcomes.

- How often should you check it? Quarterly

Buyout Report

- What is it? Compares your committed costs against your estimated costs and shows what’s left to commit.

- Why bother? A good buyout report is the first step toward locking in your profit margins on a project level.

- How often should you check it? Weekly or even daily on smaller projects, until subcontracts and purchase orders are mostly accounted for. You may also refer to these to improve future bids or explain the performance of a project.

Real-Time Cost Report

- What is it? Real-time overview of all your costs against the project’s budget, including estimated labor costs based on timesheets (vs. waiting for payroll to run) and pending purchase orders.

- Why bother? The purpose here is to keep an eye on your actual vs. budgeted labor costs and ad-hoc material purchases against the original budget and the project’s progress, which allows you to quickly identify and correct cost overruns and safeguard your profit margin.

- How often should you check it? As often as needed until the costs start feeling predictable

Change Order Tracker

- What is it? Compiles a list of the amounts and statuses of all change orders associated with a project.

- Why bother? When changes to requirements are unaccounted for, you lose money. Having a report specific to tracking change orders and their status encourages the same amount of scrutiny on additional work as was on the original quote.

- How often should you check it? At least Weekly

How to Make Construction Reporting Easier

The truth is, the construction industry is full of unique challenges in how money is tracked, earned and collected, which is why so many contractors struggle to create a clean reporting process that is accurate and consistent.

You need three things to make sure these reports stay up-to-date and accurate:

- Processes and/or tools that make data collection faster. That means a time-tracking tool that integrates with your accounting tool (or an application that does both). It means making sure your project management software can cleanly integrate with your accounting software so materials can be added to your budget automatically. The list goes on but the more you can automate data collection, the more consistent and timely you’ll be able to be.

- Report templates or software that standardize the data needed. The trouble with construction is that most generic software doesn’t quite do everything you need, so you’ve got two options: Spend time making some excel templates that are simple to use and easy to read for each of these reports, then put them all together so you can easily access them on a weekly, monthly and quarterly basis. Tons of contractors do this and it can work really well while your business is still in its beginning stages. The second option is to invest in software. This is the next step when you’ve moved beyond excel. Just make sure to find one that can handle things like retainage and change orders so you’re not stuck still doing a bunch of manual work.

- A regular cadence for checking and acting upon reports. Looking at reports regularly is a habit that needs to be built. Set a day of the week that makes sense with the rest of your process where you can review the reports, take down action items and then delegate those items to the rest of your team. Then the next week, review what’s been done to move those items forward before you review your reports again.

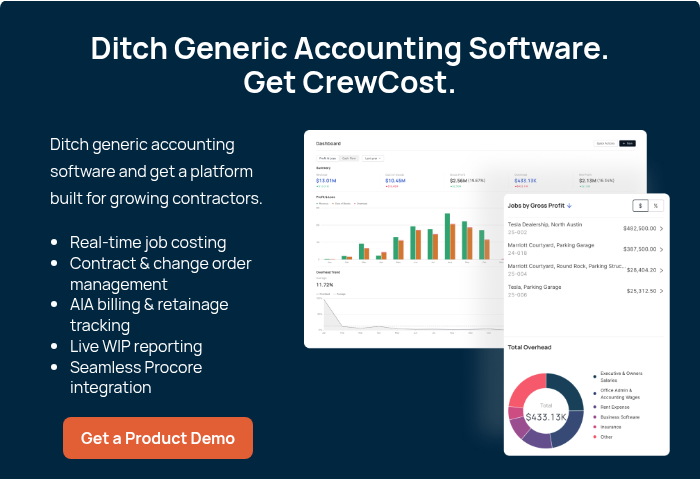

If you’re ready to move past spreadsheets, check out the solution we built specifically for contractors.