Forming solid construction accounting processes is absolutely critical if you want to grow your contracting business. The problem is, construction accounting is entirely different from accounting in other industries. From long term contracts and historically slow pay cycles to balancing costs in dynamic and unpredictable site conditions, there are a ton of factors that make financial management much more difficult. If you want to succeed, you can’t approach construction accounting from a conventional perspective.

If you’re an emerging contractor still wrestling with the unique challenges of construction accounting, this guide will make sure you’re equipped with the tools to make sound financial decisions. Consider this resource a jumping-off point — we’ll outline the basics and point you toward more in-depth guides on each topic covered so you can keep your construction company moving forward.

Key Takeaways

- Even though we follow generally accepted accounting principles (GAAP), accounting looks a lot different in the construction industry. Taking the time to learn the fundamentals of job costing, WIP reporting, etc will help your construction business maintain good financial health in the long term.

- If you’re in the beginning stages of setting up your bookkeeping system, don’t try to optimize everything at once. Incremental and intentional changes to your accounting methods can make a big impact over time.

- Accurate job costing is the single biggest thing that can help you expand your profit margins.

Essential Steps for Accurate Construction Accounting

1. Contracts and Commitments

Before any job can start, you’ll need to put a construction contract together. This lays the foundation for every aspect of work you’ll perform for clients, and outlines terms for those who will work with you. It’s also essential to controlling costs on the job. A good construction accounting system should be able to capture the basics of each new contract, including:

- A job’s start date and end date

- Who the customer is (or who the subcontractor is downstream)

- Project location

- Total contract amount

- Cost for you to perform the work (the budget)

- Retainage percentage

- Whether or not the project is taxable

- When billings are due

With this information in your accounting system, tracking things like retainage and change orders, issuing purchase orders or subcontracts, and keeping client billings on schedule becomes much easier. You’ll also use the contract’s total cost and scope of work to develop the project’s schedule of values, which breaks down individual billable tasks and their value.

🔎 Learn more about the types of construction contracts.

2. Job Costing

Because construction is project-based, you need a way to see how well individual projects are performing at a granular level, instead of trying to get a grip on your company’s financials from five miles above. This is where job costing comes in, allowing you to make sure each new construction job you take on is hitting all the marks.

Put simply, job costing is about tracking a specific construction project’s direct and indirect costs, revenue, and profit margin. It should also be integrated across your company (it’s not just your project management team’s job!) and worked into your company’s general ledger to ensure the revenue and costs on the job cost ledger align with those on your income statement.

Several things should go into your job costing process, including:

- Fully burdened labor cost

- Overhead allocations

- Direct costs on each construction job

The better you’re able to integrate all the elements that affect your profitability, the better you’ll become at project management, estimating future jobs, and controlling costs on and off the job site. If you want to grow sustainably, this is a construction accounting principle you have to master.

3. Percentage of Completion Method

Maintaining a healthy business also means learning how to correctly recognize and report your revenue. There are four revenue recognition methods, but for the sake of this guide, we’re going to focus on the percentage of completion method (POC), which is what most contractors end up using.

This method is particularly helpful on long-term projects, and can help you ensure that reported revenue and cost numbers match as closely as possible with the actual billing and spending on the job. You can use a few different methods to calculate POC, although the most commonly used approach is the cost-to-cost method, which works like this:

Cost to Date / Total Project Costs = POC

Let’s say you have $50,000 in current expenses on a project estimated with $250,000 total contract costs. Using this formula, the percentage of completion calculation would be:

$50,000 Cost to Date / $250,000 Cost to Completion = .20, or 20% percentage of completion

You can now use this percentage to calculate the amount of revenue to recognize for a specific project milestone or pay period.

4. Progressive Billing

Keeping enough cash on hand is a serious challenge in our industry, especially on longer jobs. To maintain a positive financial position, you’ll want to use progressive billings (aka progress billings). Instead of a lump sum at the end, progress payments are made in regular installments (usually monthly) as a project progresses.

Each payment is tied to a payment application. In simple terms, this just means that however much work you’ve done determines what you can bill based on the contract price. It’s a simple process: When you’re ready to bill, request a payment via a payment application, and include any other forms required by the construction contract. Once sent, all you have to do is wait to be paid. With progressive billing, you’ll be able to spot cash flow and payment issues pretty quickly. If payments stop coming through, you may be able to stop work until the problem is resolved.

🔎 Want to learn more? We wrote an entire guide to progress payments you can check out.

5. Change Order Management

A surefire way to lose out on project profitability is to do work you’re not paid for. An effective change order management system is your first line of defense against this. Your change order system should track a potential change from the moment the issue is identified to the end (whether a change order was actually issued for the work or not).

With this system in place, you’ll be able to see:

- If any additional costs were captured correctly in your accounting

- If you received enough revenue to offset that cost - and hopefully profit from the situation

Having this kind of system for every construction contract you take on is essential. Once in place, it will not only help you ensure your original estimate was correct but confirm you’ve accurately captured the scope of the project based on what you’ve bid.

6. WIP Reporting

It’s hard to protect your margins on the job without being able to see how it’s performing in real-time. WIP reports make it easier to get an overview of each project’s budget, percent complete, actual costs to date, and more, so you can see if it’s overbilled or underbilled.

Essentially, WIPs work to combine all your job costing in one place, so you can get both a bird’s eye view of all open jobs, and a granular look into how each one is individually performing. If you want to be able to plan better, and proactively address problems before they eat into your profit, you need this document.

Learn more about using WIP reports for effective construction management.

7. Understanding Retainage

Holding back retainage is standard on most construction jobs, especially long-term contracts. If it’s not reimbursed quickly enough though, it can cause a domino effect of cash flow problems. To properly record and track retainage, you’ll need to include an account for retainage receivables on your company’s Chart of Accounts. Next, make sure all retainage is accurately represented on your balance sheet.

You can avoid a fair bit of cash flow problems by negotiating more favorable retainage rates/terms with project owners. For example, instead of a fixed 10% holdback on each progress billing, you might negotiate terms that reduce that rate to 5% once the job reaches the halfway point. Like with most things in construction, good communication between you and the owner, along with any subcontractors or vendors will keep everyone on the same page when it comes to progress, payment status, and any changes in job scope.

Here’s more on retainage best practices.

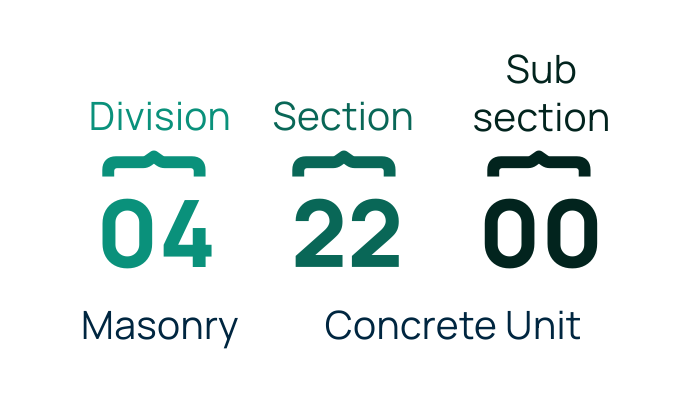

8. Cost Codes and Cost Types for Organizing Expenses

An important part of job costing is setting up an internal tracking system for project costs. The foundation of this is cost codes and cost types. You can start by categorizing all the costs it takes to complete a project (or your scope of it). Think of it like this: job > phase > cost code > cost type.

Cost codes: These are specific budget categories for project expenses, and are set up like this:

Cost types: Include labor, materials, subcontractors, equipment, and other categories.

To actually be effective, your cost coding system needs to be used consistently by everyone in your company. This ensures accurate and consistent data entry that will ultimately help you bid better on future projects.

See our job costing guide for more info on organizing project expenses.

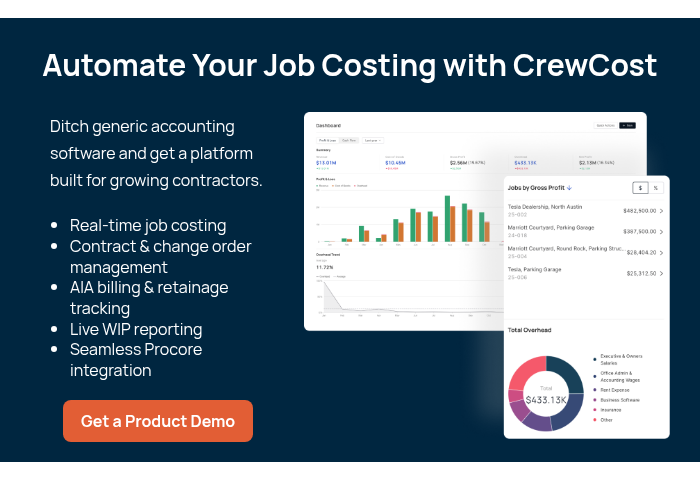

9. Construction Accounting Software

Ideally, each of your financial accounting processes should work together seamlessly as a part of a larger system. A construction accounting software makes this level of integration simple, so you can keep track of everything and enable more informed decision-making as time goes on.

At CrewCost, our construction accounting platform was made by contractors, for contractors, so you can build confidently without tons of workarounds. CrewCost brings all your financial data into one place, so you can fully optimize your operations and build more profitabily. You'll get tools like:

- Customizable financial reporting

- Customized financial statements for construction

- Easy project cost tracking

- Overhead cost tracking

- Real-time insights into your business

- Automated time tracking

- Cash flow forecasting

Learn more about our purpose-built accounting solutions here.

Wrapping Up

The first step to building more accurate accounting processes is recognizing that construction accounting is different. It’s definitely a mindset shift, but the good news is, no matter what kind of contractor you are, your construction firm's needs are going to look pretty much the same. It’s how (and how much) you lean into practices like WIP reporting and job costing that will ultimately begin to move the needle for you.

Of course, if you want to make your life easier, construction accounting software like CrewCost will do a lot of the heavy lifting for you. Schedule a demo today!